The past three years have been tough for fixed income investors. Rapidly increasing interest rates and stickier-than-anticipated inflation created a volatile return environment—an unwelcome surprise in an asset class that most investors expect to serve as the “boring” part of their portfolio.

The silver lining of this volatility? Fixed income securities finally offer meaningful yields. That’s a big change from the near-zero yields bonds have offered over the past decade. Despite higher yields, the negative return environment of 2021 and 2022 remains top of mind for many advisors: They remain cautious about allocating their clients’ portfolios back to bonds.

Cash may not be king

If you’ve been keeping cash on the sidelines since 2022’s extreme tumult in the fixed income market, you’re not alone. Money market assets under management are at an all-time high relative to the past 30 years. But today’s high yields and a shifting focus for the Federal Reserve may change the equation.

Higher starting yields on bonds can help provide your clients with a larger cushion against future price declines if rates increase. And while cash pays a high yield today, rate cuts expected in the year ahead suggest that high yields may not be here for long. Treasury bonds may give your clients a way to get back into the fixed income market. They can lock in higher yields for longer while introducing a ballast against an equity downturn in their portfolio.

Why Treasuries offer better value now

Bond investors likely saw yields rise to their highest point last fall. The yield on the 10-year U.S. Treasury note began 2023 at 3.34%. It rose to 5% in mid-October before falling back to under 4% by year-end.

The market has begun to focus on determining the frequency and pace of rate cuts in the years ahead. That means you have an opportunity to lock in higher-than-average Treasury yields and protect your clients’ portfolios now.

In our fixed income outlook for the first quarter of 2024, we estimate rates will ultimately settle above the levels we saw after the 2008 global financial crisis, which were unusually low. Yields across fixed income markets have increased and credit spreads across sectors are tight, offering investors less additional return over nominal returns. With this backdrop, Treasury bonds can provide your clients with some protection during a bear market flight to safety, without sacrificing a high amount of yield.

We find that even when advisors have maintained their fixed income exposure, their portfolios are often underweight in Treasuries. In 2023, nearly 70% of advisor portfolios underweighted Treasuries compared with the Bloomberg U.S. Universal Index, according to an analysis of 1,178 fixed income portfolios by Vanguard Advisor Portfolio Analytics and Consulting.

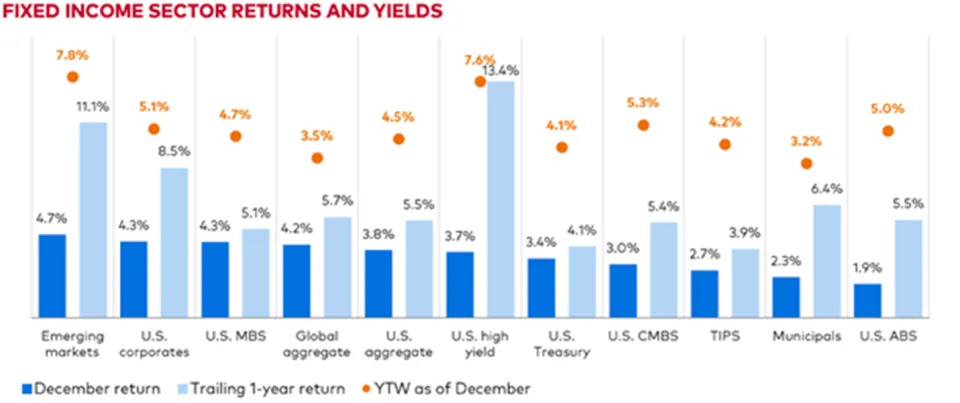

A series of bar-and-dot charts showing December 2023 returns, trailing 1-year returns as of December 31, 2023, and yields to worst as of December 31, 2023, for several taxable fixed income sectors.

Emerging markets bonds had a December return of 4.7%, a trailing 1-year return of 11.1%, and yield to worst of 7.8%; U.S. corporate bonds had a December return of 4.3%, trailing 1-year return of 8.5%, and yield to worst of 5.1%; U.S. mortgage-backed securities had a December return of 4.3%, trailing 1-year return of 5.1%, and yield to worst of 4.7%; global aggregate bonds had a December return of 4.2%, trailing 1-year return of 5.7%, and yield to worst of 3.5%; U.S. aggregate bonds had a December return of 3.8%, trailing 1-year return of 5.5%, and yield to worst of 4.5%; U.S. high-yield bonds had a December return of 3.7%, a trailing 1-year return of 13.4%, and yield to worst of 7.6%; U.S. Treasuries had a December return of 3.4%, trailing 1-year return of 4.1%, and yield to worst of 4.1%; U.S. commercial mortgage-backed securities had a December return of 3.0%, trailing 1-year return of 5.4%, and yield to worst of 5.3%; Treasury Inflation-Protected Securities had a December return of 2.7%, trailing 1-year return of 3.9%, and yield to worst of 4.2%; municipal bonds had a December return of 2.3%, trailing 1-year return of 6.4%, and yield to worst of 3.2; U.S. asset-backed securities had a December return of 1.9%, trailing 1-year return of 5.5%, and yield to worst of 5.0%

Notes: The municipal tax-equivalent yield is calculated using a 40.8% tax bracket, which includes a 37.0% top federal marginal income tax rate and the 3.8% Net Investment Income Tax to fund Medicare.

Sources : Bloomberg indexes and JP Morgan EMBI Global Diversified Index, as of December 31, 2023.

Past performance is no guarantee of future returns. The performance of an index isn't an exact representation of any particular investment, as you can't invest directly in an index.

Cover the Treasury spectrum with just four low-cost Vanguard ETFs®

We designed our Treasury ETF lineup with four funds as building blocks so that you can construct efficient, straightforward, low-cost portfolios.

With this suite of Vanguard U.S. Treasury ETFs, you can tailor portfolios to individual clients and accomplish a wide range of goals:

Vanguard's approach, reputation, and scale confer significant benefits to you and your clients:

Get lower costs in more ways than one

You can always count on us to strive to help your clients keep more of their money in their pockets. Our suite of Treasury ETFs accomplishes this in two ways.

Cost advantage number one: Because our Treasury ETFs are so liquid, it’s less expensive to buy the ETF (in terms of bid-ask spread) than to buy the individual bonds. Our lower trading costs offset 50% to 100% of the ETF's expense ratio for your clients.

Bid-ask spreads of Vanguard Treasury ETFs compared with underlying bonds

|

Vanguard ETF |

ETF bid-ask spread |

Underlying securities' spread |

ETF expense ratio |

|

Short-Term Treasury ETF (VGSH) |

2 basis points |

4 basis points |

4 basis points |

|

Intermediate-Term Treasury (VGIT) |

2 basis points |

5 basis points |

4 basis points |

|

Long-Term Treasury (VGLT) |

4 basis points |

13 basis points |

4 basis points |

|

Extended Duration Treasury ETF (EDV) |

9 basis points |

41 |

6 basis points |

Source : Bloomberg Finance LP as of January 31, 2024.

Note

: Vanguard estimated the underlying bond bid-ask spread using Bond Liquidity Analysis, a proprietary calculation that uses Bloomberg data to estimate an aggregated bid-ask spread for the underlying portfolio of bonds for the 20 trading days ended January 31, 2024.

Cost advantage number two: Besides tight bid-ask spreads, Vanguard's expense ratios beat the industry average by a significant margin across maturities:

Expense ratios of Vanguard funds compared with the Lipper peer averages

|

Vanguard ETF |

Fund expense ratio |

Lipper peer average |

|

Short-Term Treasury (VGSH) |

4 basis points |

33.1 basis points |

|

Intermediate-Term Treasury (VGIT) |

4 basis points |

20.9 basis points |

|

Long-Term Treasury (VGLT) |

4 basis points |

20.9 basis points |

|

Extended Duration Treasury ETF (EDV) |

6 basis points |

20.9 basis points |

What's the bottom line?

Markets are always unpredictable, but current Treasury yields look strong. Higher yields across fixed income markets historically have provided more of a cushion against negative returns. Given that many advisors underweighted Treasuries, you may want to consider adding to your allocations to lock in rates that are relatively high.

Notes:

Permalink | © Copyright 2024 etf.com. All rights reserved